BREAKING: New York City Council Passes First of Its Kind GHG Emissions Cap for Buildings – Local Law 97

New York City Council on Thursday voted to approve Intro. 1253-C (which would later become Local Law 97), an annual cap on greenhouse gas emissions for buildings in the city. On May 18th, Intro 1253 was passed into law as Local Law 97 of 2019, with the annual reporting requirement starting in 2024, including severe penalties for over-emitting. The first of its kind law exempts certain buildings (e.g. NYCHA, rent-regulated housing, city buildings) and allows exemptions for demonstrated “financial hardships”, but does provide prescriptive measures that need to be completed by exempted buildings. Read on to learn more about the fines for non-compliance, allowable deductions, and potential impacts (i.e. increased utility rates) likely in the future.

First introduced as Intro. 1745 in October 2017, the newly passed Intro. 1253-C (later known as Local Law 97) has been in discussion and under review for the past 18 months. The Urban Green Council organized its 80×50 Buildings Partnership, comprised of energy market experts and consultants (including EnergyWatch), commercial and residential owners/managers, religious organizations, social justice community advocates, institutions, and more, in order to provide feedback on the first draft of the law and help draft a law to plausibly reach 80% emissions reductions by 2050. While some recommendations outlined in The Blueprint for Efficiency were included in new drafts of the law, the newly passed Local Law 97 is not radically different than the first version introduced back in October 2017. Building types are thankfully more segmented, the first year of compliance was pushed from 2022 to 2024, a carbon trading feasibility study will be conducted, and there are prescriptive requirements for exempted buildings. However, there are still many less than ideal components of the law that we’ll discuss below.

GHG Emissions Caps and Reporting Requirements

Penalties

Allowable Deductions such as RECs and Storage

Preparing for the Future

GHG Emissions Caps and Reporting Requirements

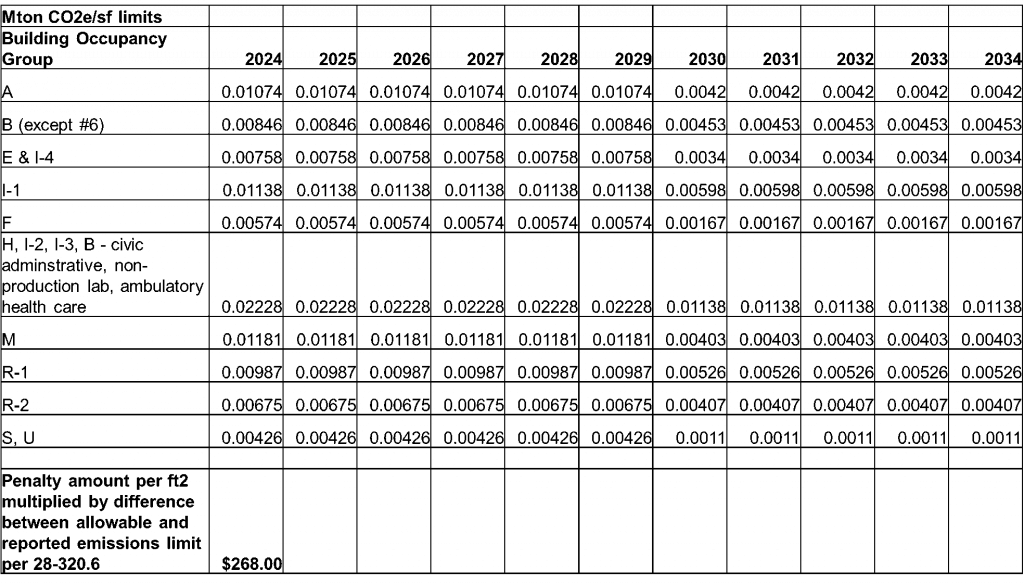

Beginning in 2024, and annually through 2029, buildings in various segmented occupancy groups will need to comply with certain published emissions intensity limits per square foot. Additional lower limits are published for 2030 through 2034, with a newly created “Advisory Board” tasked with creating limits for 2035 through 2050 (to be published before January 1, 2023). GHG emissions coefficients for electricity, natural gas, #2 and #4 fuel oil, and district steam are provided for use in calculation emissions for 2024-2029. Coefficients for the remaining years (2030 to 2050) are to be published by January 1, 2023, with factors for 2035 through 2050 required to achieve average building emissions intensity of .0014 tCO2e/sf/yr. Below is an outline of the known caps per year through 2034 for each occupancy group:

Reports for the first year of compliance are due by May 1, 2025, and each May 1 thereafter, certified by a registered design professional.

Penalties

Failure to submit an annual report for a covered building will result in a monthly penalty of $.50 per square foot for each month the violation is not corrected.

If your building emissions per square foot are higher than the allowable limit set forth in the law, you are subject to a penalty of $268 per square foot multiplied by the difference between the emissions limit and your reported emissions. For example, a 1,000,000 square foot commercial office building (group B), has an emissions limit of .00846 tCO2e/sf/yr. If the reported emissions is .009729 (15% higher), then the annual penalty is $340,092.

There is language in the law that seems to allow for judgement calls on penalty amounts based on “the respondent’s good faith efforts to comply with the requirements of this article, including investments in energy efficiency and greenhouse gas emissions reductions before the effective date of this article”, “The respondent’s access to financial resources”, and more as outlined in 28-320.6.1.

Additionally, section 28-320.7 outlines potential adjustments to annual building emissions limits based on considerations such as “the cost of financing capital improvements necessary for strict compliance with the limit set forth in section 28-320.3 would prevent the owner of a building from earning a reasonable financial return on the use of such building”.

If your building’s 2018 emissions exceed the prescribed occupancy group building emissions limit by more than 40%, then the emissions limit for 2024-2029 will be set at 70% of the reported 2018 emissions.

Allowable Deductions

EnergyWatch’s initial participation in the Urban Green Council’s working groups for the 80×50 Buildings Partnership was focused on exploring potential alternative compliance paths, such as renewable energy purchasing and a cap and trade carbon trading system. Some of our collective recommendations made its way into the law, most did not. The law allows for deductions associated with the purchase of renewable energy credits, greenhouse gas offsets, clean distributed energy resources, and storage. Unfortunately, the language is more restricting than had been recommended by the group.

REC purchases are an allowable deduction, “provided (i) the renewable energy resource that is the source of the renewable energy credits is considered by the New York independent system operator to be a capacity resource located in or directly deliverable into zone J load zone.” There is zero renewable generation in Zone J, and will likely never be grid scale renewable generation in Zone J.

“Directly deliverable into Zone J” means a renewable resource located outside of Zone J (potentially anywhere in NYISO, PJM, ISONE) which is directly connected to Zone J via HVDC transmission. As of today, there are two transmission projects that could qualify by 2024 – Champlain Hudson Power Express, Empire State Connector – with a combined transmission capacity of 2000 MW. Renewable projects connected to these HVDC lines, with PPA agreements with NYC customers, including the bundled RECs, would be eligible for the deductions. This is more restrictive than allowing any VPPA that could wheel power into NYISO (i.e. “deliverable” into Zone J, vs. “directly deliverable”). At this point, it’s unclear how many RECs could be available by 2024, what the cost premium will be, term requirements, etc.

Additionally, there are deductions available for “clean distributed energy resources”, though there’s not much rooftop solar potential in Manhattan, and lithium ion battery storage is still not allowable by FDNY in buildings.

Preparing for the Future

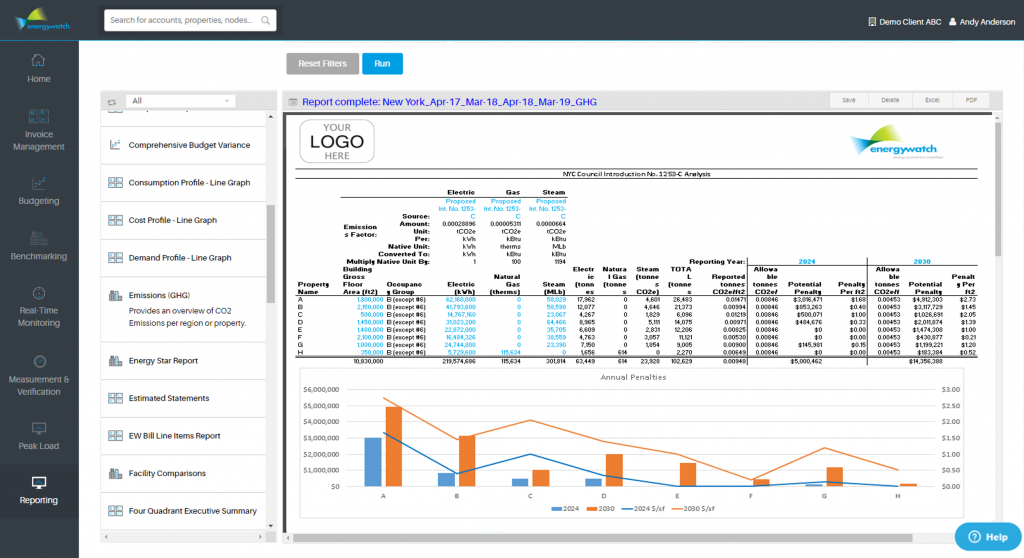

While 2024 may seem like a long way off, it’s important to understand where each of your buildings stands at this point in 2019 so you can evaluate potential future penalties, allocate budgets, evaluate financing options, and analyze strategies to reduce GHG emissions, as well as evaluate alternative compliance paths such as REC purchasing and clean distributed energy generation. EnergyWatch’s watchwire utility data management and reporting platform automatically acquires your invoice data, calculates GHG emissions based on various emission factor sets (including what’s outlined in Local Law 97), and provides reports to analyze potential penalties so we can collectively evaluate energy management and procurement options now and in the future. Contact us or take a look at our solution brief to learn more about how we can help you comply with Local Law 97.

The Role of Accountants in Sustainability Accountants are uniquely positioned to influence sustainable practices within their firms and client organizations. They have the expertise to measure and report on ESG performance, assess risks and opportunities related to sustainability, and integrate…

Finance-grade emissions data refers to emissions information that is of sufficient accuracy, completeness, and reliability to inform financial decisions. This data is crucial for: Risk Management: Identifying and quantifying climate-related risks to financial assets. Investment Decisions: Guiding investors towards sustainable…

Markets are rewarding decarbonization because decarbonization has benefits. The need for carbon data isn’t being driven by securities regulation, it is being driven by market rewards, consumer preferences, financial costs and incentives, reputational benefits, and a recognition that higher carbon…

Log In

Log In

Sustainability for Accounting Firms

Sustainability for Accounting Firms