ISO-NE Electricity Supply Rate Components: What You Need to Know

What are the component percentages in the ISO-NE?

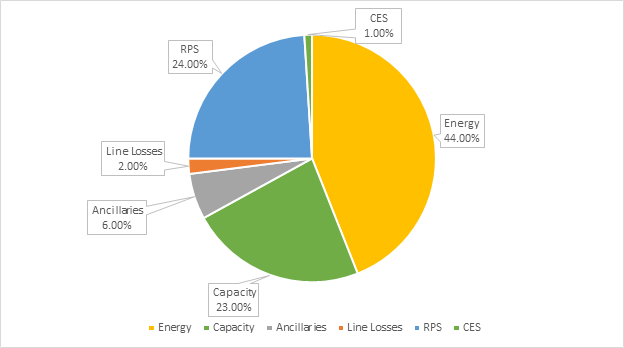

The component percentages in the ISO-NE are: 44% Energy, 24% RPS, 23% Capacity, 6% Ancillaries, 2% Line Losses, 1% CES.

How much is the energy rate a customer pays?

The energy rate a retail customer pays is determined by the type of contract secured with an ESCO. A customer will either pay variable day-ahead hourly rates (published by ISO-NE for each pricing zone), a fixed energy rate (determined by the ESCO and based on forward market pricing), or a blend of the two options.

What is RPS?

RPSs are obligations set by individual states for load-serving entities to buy a certain amount of renewable energy. This is determined by state regulated compliance percentages and the financial market for renewable energy certificates (RECs). How is capacity determined? Capacity is determined by Independent System Operator (ISO)-run auctions and customer capacity tags, which are based on their peak usage.

Currently, there are ten Regional Transmission Organizations (RTOs) in the United States. RTOs coordinate, control, and monitor multi-state electric grids. ISO New England (ISO-NE) is the independent, non-profit RTO serving Connecticut, Maine, Massachusetts, New Hampshire, Rhode Island, and Vermont (a deregulated state) . ISO-NE retail electricity supply rate components include energy, capacity, RPS, ancillaries, line losses, and CES. The component percentages, listed in the chart below, are based on Northeast Massachusetts and vary throughout New England (percentages for New Jersey can be viewed here). Percentages fluctuate based on actual kWh, ICAP/PLC, load factor and market timing.

In this article, we’ll explain each of the different supply rate components and their role in ISO-NE.

Energy – 44%

Energy, the largest supply rate component, is the actual commodity generated by power plants and consumed by customers.

98% of energy is scheduled on the day-ahead energy market, while the remaining 2% is on the real-time market.

The energy rate a retail customer pays is determined by the type of contract secured with an ESCO. A customer will either pay variable day-ahead hourly rates (published by ISO-NE for each pricing zone), a fixed energy rate (determined by the ESCO and based on forward market pricing), or a blend of the two options.

The cost of procuring energy comes from the electrons transmitted through T&D lines, and is largely based on the cost of natural gas for New England.

Renewable Portfolio Standards (RPSs) – 24%

RPSs are obligations set by individual states for load-serving entities to buy a certain amount of renewable energy. This is determined by state regulated compliance percentages and the financial market for renewable energy certificates (RECs). A complete listing of state RPSs can be found on the National Conference of State Legislatures website.

In 2020, all suppliers will be required to purchase a quantity of RECs equal to 15% of the total electricity they serve.

Capacity – 23%

Capacity is determined by Independent System Operator (ISO)-run auctions and customer capacity tags, which are based on their peak usage. The Forward Capacity Market (FCM) is meant to procure enough capacity to meet New England’s predicted demand by providing grid dependability and guaranteeing adequate generation for the region.

Ancillaries – 6%

Ancillaries are minor administrative charges ISO-NE bills to load-serving entities in order to operate the grid safely and reliably.

Forward and real-time operating reserves ensure that sufficient resources are available to produce electricity on short notice when an outage occurs.

Line Losses – 2%

Due to heating, energy is lost over T&D lines. Charges are included to compensate for the losses, which vary based on infrastructure, location of the end-user, and service class.

Clean Energy Standards (CES) – 1%

CESs are a mechanism to incentivize zero emission generation, e.g. hydro and nuclear power. Although they make up small percentage of supply rate components, Clean Energy Standards are more important than ever, given the push towards renewable energy use.

The Clean Peak Standard (CPS) is a mandate set by Massachusetts to encourage renewable and storage power supply during peak periods. Established as part of the 2018 Act to Advance Clean Energy, the CPS allows for qualified renewable energy generators, energy storage resources, and demand response resources to earn Clean Peak Energy Certificates (CPECs) for every megawatt hour of electricity they produce or reduce corresponding with Seasonal Peak Periods (SPPs).

CPECs can be purchased by retail electricity suppliers who are annually required to procure a certain quantity of CPECs. In 2020, retail electricity suppliers will be obligated to procure CPECs equal to 1.5% of their total electricity sales to end-use customers. This requirement increases by 1.5% each year and may increase by more if the market is oversupplied.

Since the retirement of the 680-megawatt Pilgrim Nuclear Power Station on May 31, 2019, several new resources have come online, including three dual-fuel plants capable of using either natural gas or oil to produce power, as well as solar and wind resources.

According to the season system outlook, ISO-NE develops forecasts every fall predicting consumer demand for the upcoming winter peak season of December through March. Throughout the winter, ISO-NE surveys generators on their fuel supplies, confirms daily scheduled natural gas deliveries to the region, and forecasts the expected energy availability over a 21-day period. ISO-NE also coordinates with the region’s power generators and natural gas pipeline companies ahead of the winter months to assess the region’s energy supply.

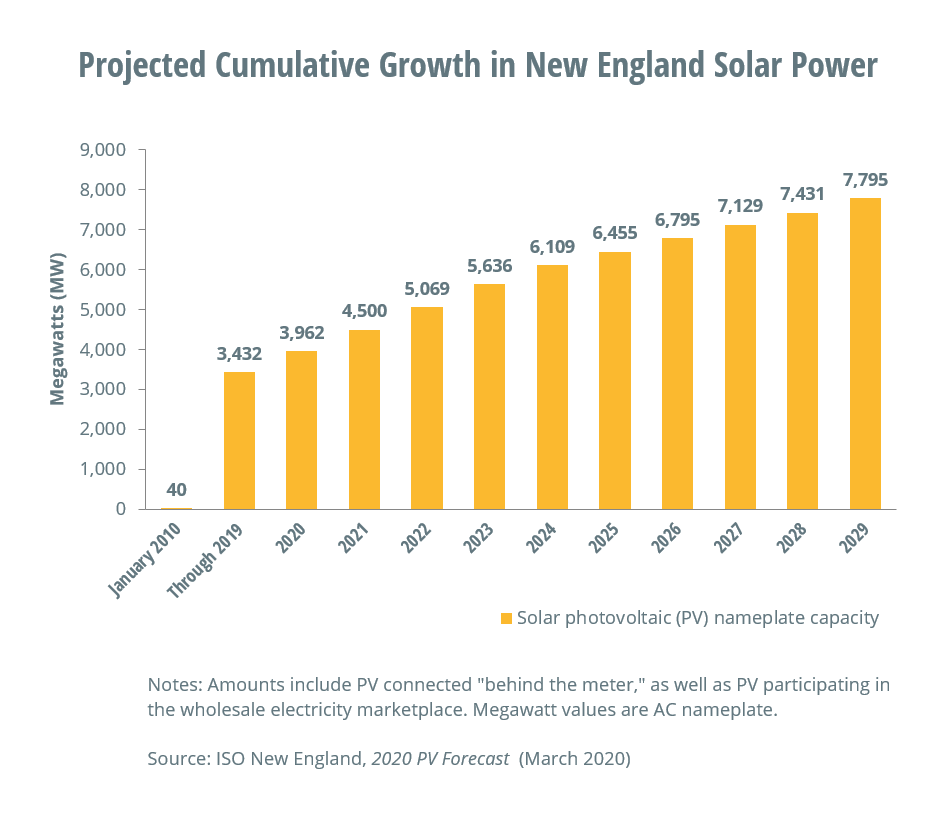

Solar power systems are rapidly being installed across New England, noticeably reducing the electricity used from the regional power system. The ISO-NE’s 2020 PV forecast anticipates 6,700 megawatts (MW) of nameplate PV capacity by 2029. As of December 2019, more than 180,000 behind-the-meter solar photovoltaic installations have been made, with the capability of generating more than 3,400 MW. The chart below shows projected growth in New England’s solar power industry.

ISO New England filed its Energy Security Improvements (ESI) proposal with the Federal Energy Regulatory Commission (FERC) on April 15, 2020. The proposal mentions that fuel security is a possible component going forward for 2022-2025.

For a more in depth review of electricity supply rate components and electricity markets in ISO-NE, click here to download EnergyWatch’s Electricity Markets Explained report.

In April, WatchWire by Tango brought together industry leaders, innovators, and clients for the second annual INTEGRATE User Conference, held at Virgin Hotels New York City. This year's conference centered on the critical theme of integrating energy and sustainability within…

Carbon Neutral Carbon neutral means that any CO2 released into the atmosphere from a company's activities is balanced by an equivalent amount being removed. Everything you do produces carbon dioxide. Being "carbon neutral" means that you, or the operations of…

The Role of Accountants in Sustainability Accountants are uniquely positioned to influence sustainable practices within their firms and client organizations. They have the expertise to measure and report on ESG performance, assess risks and opportunities related to sustainability, and integrate…

Log In

Log In

Integrating Sustainability and Energy Management: Insights from WatchWire by Tango’s Second Annual INTEGRATE User Conference

Integrating Sustainability and Energy Management: Insights from WatchWire by Tango’s Second Annual INTEGRATE User Conference