PJM Capacity Market Minimum Offer Price Rule (“MOPR”) Could Alter Market

On June 29th the Federal Energy Regulatory Committee (FERC) issued an order that could potentially change the PJM market significantly. The order primarily focused on PJM’s Minimum Offer Price Rule (“MOPR”) which sets a minimum offer price for capacity bids submitted by new generation as a means to protect against buyer-side market power. Generator interests (such as Calpine) claim the PJM MOPR is unreasonable because it fails to address the impact of subsidized resources (e.g. ZECs for nuclear generation) on the capacity market. They also argue that all resources should be subjected to the MOPR, as it would strip out the price decreasing impact of generation (renewable energy and some nuclear) that receives out of market subsidies on capacity market prices. In the order, FERC concluded that generators receiving out-of-market payments depress capacity market clearing prices by submitting artificially low offers in the PJM capacity auction and rejected various parties’ proposals, including PJM’s, as they were deemed insufficient to remedy the problem. FERC instead outlined two alternative options to be considered further:

Option 1

FERC’s first option was for PJM to develop a version of the MOPR that would apply to all new and existing resources receiving state subsidies. FERC rejected PJM’s position that would have exempted generation that is subject to state RPS requirements in PJM from the MOPR.

Option 2

FERC’s second option was for individual generation resources that receive subsidies to be able to opt out of the capacity market along with commensurate load while continuing to participate in PJM’s energy and ancillary services markets. “This option, termed “FRR Alternative” (Fixed Resource Requirement Alternative), is based on the current FRR option, which allows utilities (but not individual resources) to choose to opt out of the capacity markets, together with related load” (Beh). For generators that receive out-of-market subsidy payments, they will either become subject to the PJM MOPR or will opt out of the capacity market altogether through the FRR Alternative plan. If the generator takes the FRR Alternative route, then the generators will miss out on capacity market revenues thereby requiring the states providing the subsidy to increase those subsidies going forward. The uncertainty in revenues could also jeopardize the development of future projects if these states do not step up to fill this revenue void. On the other hand, if the generator stays in PJM’s capacity market and becomes subject to the expanded MOPR, then capacity clearing prices may increase resulting in increased cost to load. “In addition, if FERC’s concerns about price suppression are correct, and the expanded MOPR results in higher capacity prices, the cost to load of the subsidized resources may be higher because the cost of the subsidies will not be offset by lower capacity prices.”

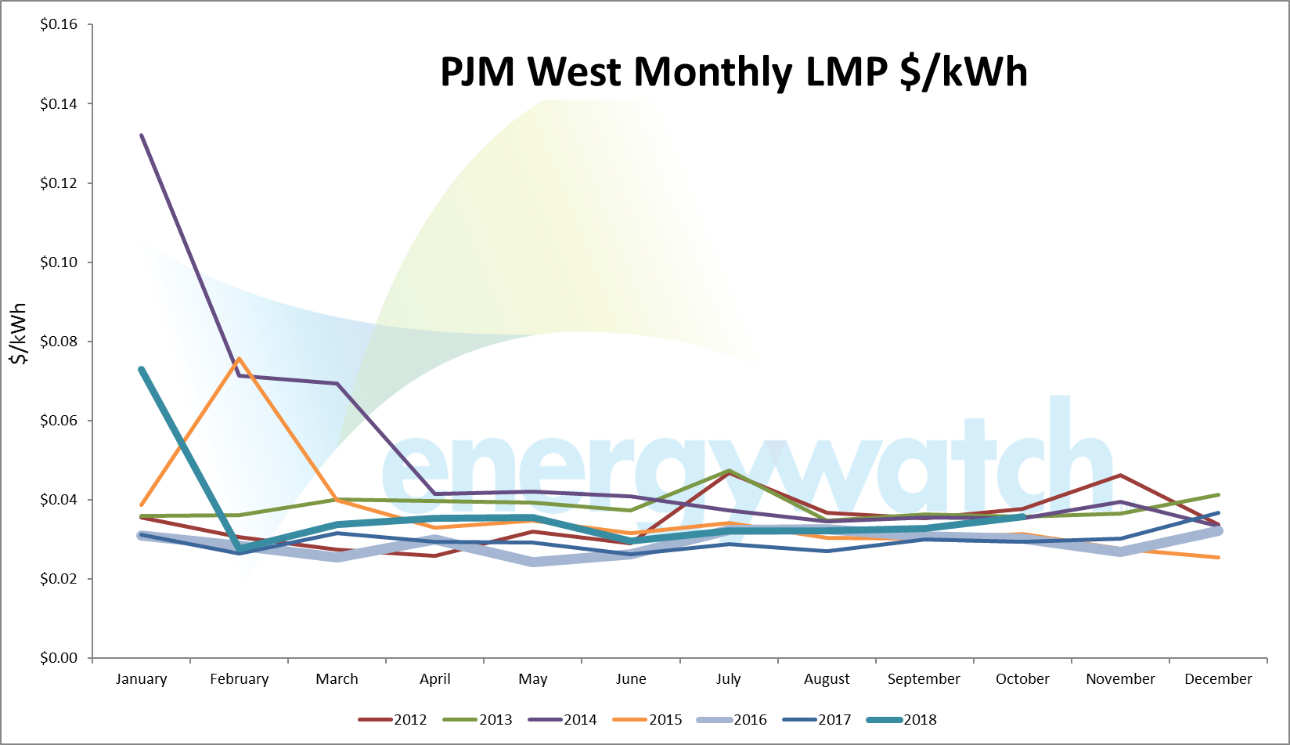

Andy Weissman’s EBW Analytics Group Energy Risk Report Conference in Philadelphia outlined a few issues with FERC’s decision on Calpine’s order. The debate has focused on the wrong issues, such as outage risks for different types of generation and the potential need to continue operating coal and nuclear units facing retirement to ensure adequate capacity reserves. The real issue at hand is the limitation on the maximum amount of gas that can be delivered to generators in PJM and other Northeastern ISO’s on a cold day since the “shale gas revolution” has played a major role in bringing down electricity prices in spring, summer and fall but greatly increases exposure to severe price spikes in winter. Extremely cold weather tests the capacity of the pipeline system and there is not enough capacity in the northeast to meet space heating and power generation demand on the coldest days of the year.

Both the 2014 Polar Vortex and the 2018 Bomb Cyclone have exemplified the severity of pipeline constraints on electricity pricing. On January 1, 2018, the coldest day of the year, 15% of total gas-fired generation in the northeast did not operate. There was not enough delivery capability for the transportation of the natural gas and, as a result, demand was not met and prices drastically increased. Last winter, the grid did not succumb to a forced outage because the coldest day occurred on a holiday. However this year’s winter season could be a larger problem if the peak occurs on a regular weekday (i.e. not a holiday), the temperature is even colder, or if the gas supply that served the northeast is committed to another region (Weissman). FERC’s new approach to pipeline additions could alleviate the issue but it will take at least 4-5 years and a reassessment of the Commission’s responsibilities. In the meantime, if the frequency of extreme weather continues to grow, then continued retirements of non-gas fired generation could lead to catastrophic results as capacity costs are increasing as a percentage of total electricity costs.

The huge price declines since 2008 due to the shale gas revolution has made it increasingly more difficult to keep supply and demand balanced. Shale formations are unable to export sufficient gas and pipeline bottlenecks led to localized oversupply in the Northeast that depressed prices. Production growth has distorted the market and incremental supply has far outpaced weather-normalized demand growth. The continued supply growth in the most likely scenario suggests a vastly oversupplied market for 2019, which can sink prices to the low $2.00/MMBtu range.

Beh, James C. Mondaq Connecting knowledge & people. (2018, August 9). FERC Finds That State-Supported Generation Resources Suppress PJM Capacity Market Prices, Establishes Proceeding To Design And Implement Broad Market Reforms. Retrieved 2018, October 8, from

The Role of Accountants in Sustainability Accountants are uniquely positioned to influence sustainable practices within their firms and client organizations. They have the expertise to measure and report on ESG performance, assess risks and opportunities related to sustainability, and integrate…

Finance-grade emissions data refers to emissions information that is of sufficient accuracy, completeness, and reliability to inform financial decisions. This data is crucial for: Risk Management: Identifying and quantifying climate-related risks to financial assets. Investment Decisions: Guiding investors towards sustainable…

Markets are rewarding decarbonization because decarbonization has benefits. The need for carbon data isn’t being driven by securities regulation, it is being driven by market rewards, consumer preferences, financial costs and incentives, reputational benefits, and a recognition that higher carbon…

Log In

Log In

Sustainability for Accounting Firms

Sustainability for Accounting Firms